Term |

Explanation |

|---|---|

13th Period |

In normal accounting practices there are twelve reporting periods in a financial year. Each of these periods is represented by a calendar month, and is a defined chronological period. The 13th period isn't an actual period of time – it's merely a place-holder period that contains year end adjustments so they don't affect a particular reporting period. |

Account |

A section in a ledger devoted to a single aspect of a business (eg. bank account, wages account, office expenses account). |

Amortisation |

The depreciation of an intangible asset (eg. loan, mortgage) over a fixed period of time. For example, if a loan of $12,000 is amortised over one year with no interest, then the monthly repayments (amortisation) would be $1000 a month. |

Arrears |

Bills which should have been paid. For example, if you have forgotten to pay your last three months' rent, then you are said to be three months in arrears on your rent. |

Assets |

Assets represent what a business owns, or is due. Equipment, vehicles, buildings, debtors, money in the bank, cash are all examples of the assets of a business. Typical breakdown includes fixed assets and current assets. Current refers to cash, money in the bank, debtors, etc. Fixed refers to assets that cannot be easily liquidated, such as equipment, buildings, plant, vehicles, etc. |

At Cost |

The at cost price usually refers to the price you originally paid for something, as opposed to the price you sell it for. |

Audit |

The process of checking every entry in a set of books to make sure they agree with the original paperwork (eg. checking a journal's entries against the original purchase and sales invoices). |

Audit Trail |

A list of transactions in the order they occurred. |

Bad Debts Account |

An account to record the value of unrecoverable customer debts. |

Balance Sheet |

A balance sheet is a snapshot of all the assets, liabilities and equity (ie. what a company owns and owes) at a point in time. |

Burn Rate |

The rate at which a company spends its money. For example, if a company had cash reserves of $120m and it was currently spending $10m a month, then you could say at the current burn rate the company will run out of cash in one year. |

Capital |

An amount of money put into the business (often by way of a loan), as opposed to money earned by the business. |

Cash Flow |

A report which shows the flow of money in and out of the business over a period of time. |

Chart of Accounts |

A list of all the accounts held in the general ledger. |

Closing the Financial Year |

A term used to describe the journal entries necessary to close the sales and expense accounts of a business at year end by posting their balances to the balance sheet. |

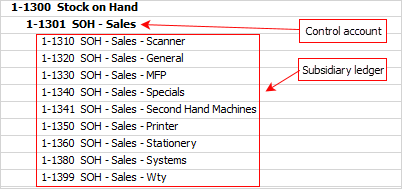

Control Account |

A general ledger header account containing the correct total amount without containing the details. The actual details are found in the subsidiary ledger. For example, the Cash On Hand control account would merely update with a few amounts, such as total collections for the day, etc. The details on each customer and transaction would not be recorded in this account. Rather, these details will be in the Cash On Hand subsidiary ledger.

|

Cost of Goods Sold (COGS) |

The COGS are the true cost of goods plus any other direct expenses incurred in preparing the goods for sale. |

Credit |

An accounting entry that either increases a liability or equity account or decreases an asset or expense account. |

Creditors |

A list of suppliers to whom the business owes money. |

Debit |

An accounting entry that either increases an asset or expense account or decreases a liability or equity account. |

Debtors |

A list of customers who owe money to the business. |

Depreciation |

The value of assets usually decreases as time goes by. The amount or percentage that it decreases by is called depreciation. It is shown in both the profit & loss account, and balance sheet of a business. |

Double entry book-keeping |

A system which accounts for every aspect of a transaction – where it came from and where it went to. This from and to aspect of a transaction is called crediting and debiting, which is what the term double entry means. |

Entry |

Part of a transaction recorded in a journal or posted to a ledger. |

Expenses |

Goods or services purchased directly for the running of the business, ie. stationery. This does not include goods bought for resale or any items of a capital nature. |

First In First Out (FIFO) |

A method of valuing stock, ie. the oldest inventory items are recorded as sold first, but do not necessarily mean that the exact oldest physical object has been tracked and sold. In other words, the cost associated with the inventory that was purchased first is the cost expensed first. |

Fixed Assets |

These consist of anything that a business owns or buys for use within the business and that still retains a value at year end. They usually consist of major items such as land, buildings, equipment and vehicles, but can include smaller items, like tools. |

Fiscal Year |

The term used for a business accounting year or financial year. The period is usually twelve months, which can begin during any month of the calendar year (eg. 1 July 2017 to 30 June 2018). |

GL Accounts |

A set of accounts held in the general ledger. |

General Ledger |

A ledger (or area within accounting software) which holds all the GL accounts of a business. |

Fixtures & Fittings |

This is a class of fixed asset which includes office furniture, filing cabinets, display cases, warehouse shelving, etc. |

Income |

Money received by a business from its commercial activities. |

Intangible Assets |

Assets of a non-physical or financial nature. Assets such as a loan or an endowment policy are good examples. |

Inventory |

A subsidiary ledger which is usually used to record the details of individual items of stock. Inventories can also be used to hold the details of other assets of a business. |

Invoice |

A term describing an original document, either issued by a business for the sale of goods on credit (a sales invoice) or received by the business for goods bought (a purchase invoice). |

Journal(s) |

The place where your transactions are first entered. |

Journal Entries |

A term used to describe the transactions recorded in a journal. |

Ledger |

The place where entries posted from the journals are reorganised into accounts. |

Margin |

Margin is sales minus the cost of goods sold. For example, if a product sells for $100 and costs $70 to manufacture, its margin is $30. Or, stated as a percentage, the margin percentage is 30% (calculated as the margin divided by sales). |

Markup |

Markup is the amount by which the cost of a product is increased in order to derive the selling price. For example, a markup of $30 from $70 yields a selling price of $100. Or, stated as a percentage, the markup percentage is 42.9% (calculated as the markup amount divided by the product cost). |

Petty Cash |

A small amount of money held in reserve – normally used to purchase items of small value where a cheque or other form of payment is not suitable, eg. coffee for the office, etc. |

Point of Sale (POS) |

The place where a sale of goods takes place, eg. a shop counter with a till. |

Posting |

|

Profit Margin |

The percentage difference between the cost of a product and the price you sell it for. For example, if a product costs you $10 to buy and you sell it for $20, then you have a 100% profit margin. |

Reconciling |

The procedure of checking entries made in a company's books with those on a statement sent by a third person (eg. checking a bank statement against your own records). |

RAI-US / RAI-NR |

Return as is literally means the item being returned is not repairable, or cannot reasonably be repaired. The differentiation here is between service that is stopped for whatever reason, not repairable (RAI-NR), or not completed because the product is unserviceable (RAI-US). |

RFC |

|

RTV |

|

Stock |

Goods manufactured or bought for resale by a business. |

Stock Taking (Stocktaking) |

Stocktaking or inventory checking is the physical verification of the quantities and condition of items held in an inventory or warehouse. This may be done to provide an audit of existing stock. It is also the source of stock discrepancy information. |

Tangible Assets |

Assets of a physical nature. Examples include buildings, motor vehicles, plant and equipment, fixtures and fittings. |

Further information: